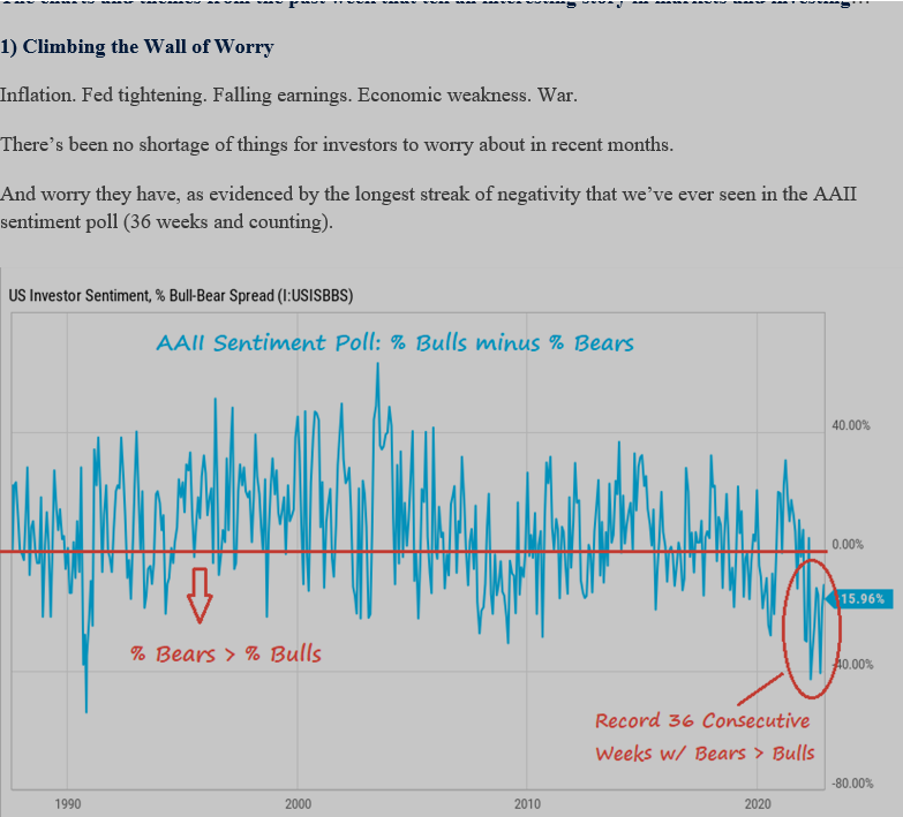

Play 4CRB Radio Segment: ‘What to consider when thinking of leaving the family home’ with Troy Theobald of RFS Advice

Why do people normally consider leaving their home?

- The home is just too large

- You want to free up capital to pay for your ideal lifestyle

- The ongoing upkeep can be too much

- It has stairs

- There can be a loss of independence

- The loss of a drivers licence or mobility

- There could be the passing of a spouse

- They do not feel safe in their current location

What options are there?

Stay in the home

Try and access either some government assistance for in-home care or start to pay for some help. It could be the garden or housekeeping, or it could be more advanced, like assistance with getting to doctor’s appointments, or help with the shopping, or even daily activities like showering or meal preparation.

Currently there are two distinct government programs that operate to facilitate this care: the Commonwealth Home Support program (which covers the most basic types of assistance like occasional garden maintenance or deep cleaning of the house occasionally) and the Home Care Program, which at present has four levels of care and provides a budget that can be used at the discretion of the recipient.

Unit

This may be smaller than the family home and feel more secure. It may even be a gated community.

It will have less upkeep – some of the outside maintenance may be done by the body corporate

It can provide a sense of community which can be good or bad.

Retirement villages or Over 50’s villages

Retirement villages or Over 50’s villages are likely to provide a greater sense of community than merely downsizing into a unit, because they bring together people who are of similar life-stage with the particular goal of enjoying the community activities such as bowls/tennis/croquet etc. Although this particular aspect of retirement villages and Over 50’s villages overlaps, the two are quite different from a financial perspective, and actually run under two different sets of legislation.

A retirement village will generally be a leasehold arrangement (although there are variations on this) whereby you purchase the right to reside in the property for an extended period of time, and when you leave the village, there will be a Deferred Management Fee deducted from the ingoing contribution that was paid. In addition, there are ongoing weekly fees to maintain the communal facilities.

An Over 50’s village is run under the Manufactured Homes (Residential Parks) Act and can sometimes be called a Land Lease community. Within these communities you would own the actual house, but leave the site on which the house sits. The weekly payment of site fees, can qualify one for rental assistance if you receive an Age Pension or part Age Pension.

Independent living units with care on site

There are some retirement communities that offer additional benefits (over and above the usual ones) such as having care provided on site.

There are a variety of offerings out there, and it could be as simple as having cleaning and meals provided, or there could be the option to have further services provided by an on-site provider either paid for privately or funded by way of a home care package.

This can sometimes be an alternative to residential Aged Care.

Move in with the kids

Moving in with the kids can sometimes be an option, although I would strongly urge that families try this on a temporary basis before committing funds or assets to make this a permanent arrangement.

Coming from a family that had four generations under the same roof at one point, I can honestly say that it has some amazing benefits but it also has some substantial challenges, and it can be a very costly mistake if things don’t work out the way that everybody hopes.

We would always suggest getting some legal and financial advice before taking this step.

When we say Granny Flat – most people will think of a small apartment that is a sectioned of piece of the kids’ home or even slightly apart from the main house, but on the same property. This is the real estate definition of a Granny Flat.

The Social Security definition of a Granny Flat Right is somewhat different, and is essentially a gifting concession within certain rules and limits. The fundamental principle behind the Granny Flat Right is that you can provide a monetary benefit to family members in exchange for the right to reside in the home and receive care. But be warned there are some substantial pitfalls.

What are the benefits to downsizing?

- Downsizing can provide an opportunity to add funds into your retirement savings pool, and may therefore provide the opportunity to enjoy more lifestyle benefits, like added travel.

- A smaller property within a community environment (whether that’s an apartment block or a unit complex or a retirement village) can be easier to lock up and go travelling, because there are close neighbours to keep an eye on things.

- You may have the benefit of communal facilities like swimming pools etc without the physical upkeep.

- There may be organised community events that allow for a fuller lifestyle and less loneliness.

- You may have chosen a community that has some care available for when you need help with things like cleaning, washing or meal preparation.

At what point in a health situation should you consider moving?

There is no rule for when the best time is to move, but awareness of our increasing care needs and the ability to confront this with an open mind can assist us to access the services that could be of benefit.

Accessing some home care can significantly increase the amount of time that we’re able to live independently at home, and reduce the likelihood of a crisis point where there is a fall with a trip to hospital that can result in less choices being available.

What services are out there to help them consider different options?

In all of the accommodation options we touched on there is the option to access some form of home care through either the Commonwealth Home Support Program (which is funded through organisations that provide the services in their local area); OR if a higher level of support is required, through a Home Care Package.

In the next few years, these two programs will merge. In the meantime, you can access either program by calling myagedcare (1800 200 422).

The first step in the process is an assessment – this is like an interview with a member of the ACAT team, wherein they will assess needs and urgency.

So, for example, someone who has mobility difficulties and not much family support nearby is likely in a more urgent category than someone who has lots of family support who is still fully mobile.

A change in lifestyle, like a downsizing move into whichever accommodation option you may choose, may have both financial and potential estate planning consequences.

A financial planner who specialises in retirement funding/living can assist in finding the right pathway forward for your personal circumstances, and the services of an appropriate legal professional may also be required.

What service does RFS Advice aged care normally offer?

We can assist in comparing various options for your future from a financial perspective – whether that’s a move into a retirement village, downsizing and adding money into the retirement savings pool, or even entering residential aged care.

We specialise in assisting with the financial implications of accessing all types of care, and can make recommendations that help you avoid certain pitfalls which can be very costly in the long term.

We will help you gain a clear picture of your potential future cashflow or income as well as your asset position over time.

We will help you find a sustainable way to fund your retirement and meet the care needs that progressively increase along that journey.

What factors should you consider?

There are both financial and lifestyle factors to be considered

Financial

- How much should you spend

- What will you do with the remainder

- How will that affect Centrelink benefits?

- Will I outlive my capital?

Lifestyle

- What location do you want to live in?

- Is it near shops/doctors/clubs that you usually frequent?

- Do you have family nearby?

- Do you have friends in the same community?

What happens when care needs escalate and ill health determines that there is a need to move into Residential Aged Care?

Residential Aged Care can be quite confusing especially from a financial perspective, and it’s possible to make decisions that can have some significantly negative impacts on personal wealth. How you structure assets can affect how much you pay in fees, so it’s always a good idea to talk to someone who specialises in financial advice in this particular area.

The government regulates the fees for residential aged care. How much you pay may depend on:

- Your chosen aged care service

- Your assessable assets and income (which may include Centrelink age pension or Veterans’ Affairs (DVA) benefits) as assessed by Services Australia.

The range of fees is shown in the diagram below.

The Government may provide support in helping you pay for your accommodation and means-tested care fees. To determine your level of support, you will need to complete an income and assets assessment by submitting a ‘Residential Aged Care Property details for Centrelink and DVA Customers form (SA485)’ form (or online version SA486 form) to Services Australia. If you receive a means-tested pension you will need to ensure that your income and assets details and personal circumstances are up to date with Centrelink before submitting.

Assessable income includes income assessed under the Centrelink income test plus assessable Centrelink payments. Assessable assets include assets assessed under the Centrelink assets test plus amounts paid towards the RAD plus the capped value of the home of $186,331.

Tips and tricks

- Get some financial advice before making the big decisions.

- Think about the estate planning consequences ahead of time and whether you need to review anything like Wills or Powers of Attorney.

- If you’re going to be accessing some kind of care services, compare a few providers before deciding which to use.

- If you’re selecting a Home Care provider, ask about their package management fees, ask about their hourly rates and whether there is a minimum amount of time that a carer will be required to spend with you in a single block (this can make the package somewhat less flexible). Ask whether you will have the same carer each time.

More in-depth technical:

Home care

The government subsidises care in your home through a home care package. To be eligible you will need a valid ACAT assessment for home care which will specify the level of care (from 1 to 4) that you are eligible for.

If approved, your name is added to the National Queue until a package is available and ready to be allocated to you. At this point you will receive a letter with a referral code that you can give to your selected home care provider to release the available funds. It is important that you take these steps within the timeframe specified in the letter or your allocation may be cancelled and you could be placed back on the bottom of the queue.

You can start your research by searching the list of home care providers on www.myagedcare.gov.au

The cost of a home care package includes a basic daily fee and an income-tested fee. All recipients can be asked to pay the basic fee. Some providers may waive this fee, but that then reduces the value of the package to you.

The basic daily fee and maximum government subsidy depends on the package level. These amounts are indexed six-monthly for the basic fee and annually for the subsidy. Current rates are shown in the table below.

| Package Level | Basic daily fee per day | Subsidy per day | Total per annum |

| Level 1 | $10.49 | $25.15 | $13,008.60 |

| Level 2 | $11.09 | $44.24 | $20,195.45 |

| Level 3 | $11.40 | $96.27 | $39,299.55 |

| Level 4 | $11.71 | $145.94 | $57,542.25 |

How much you are asked to pay as an income-tested fee depends on your assessable income as calculated by Services Australia (SA). Full age-pensioners will not be asked to pay this fee, but part-pensioners and self-funded retirees could be asked to pay up to $33.60 per day. Each dollar you pay reduces the relevant government subsidy so it does not change the above package values, it just impacts how much of the cost you pay.

Any amounts you pay as an income-tested fee will also count towards your lifetime care cap (currently $73,378 but indexed). This may help to control costs across both home care and residential care over your lifetime.

After you start to receive a home care package, SA will calculate the income-tested fee and advise you and the care provider accordingly. This is calculated using your Centrelink or Veterans’ Affairs records (so ensure they are up to date) but if you are a self-funded retiree you need to complete the Home care package calculation cost of your care form (SA456) to advise SA of your financial details. If you do not complete this form you may be asked to pay the full package value until you reach the annual cap on the income-tested fee portion. The income-tested fee is reviewed and reassessed every quarter.

A home care package provides a set level of funding towards your cost of care. Some of these costs will need to be allocated towards the administration and co-ordination costs of your package. In some cases, the remaining budget may not be sufficient to fully meet your care needs. The extra care may need to be provided by friends and family or you may need to pay for additional services.

Granny flats – features, rights & interests

Summary

A granny flat is a type of special residence. The following explains:

- the granny flat interest rules

- what a granny flat interest is

- how to value a granny flat interest.

Features of the granny flat interest rules

The granny flat interest rules recognise family arrangements that provide support for older people. The rules do NOT have any tests of age or family relationship. The rules do NOT measure or put a value on the support provided to the older person.

The granny flat interest rules DO reduce the effect of the deprivation (gifting) rules where people transfer property or other assets to family members in return for a life interest or right to accommodation for life.

Note: It is recommended that financial and legal advice be sought before establishing a granny flat interest.

Defining a granny flat interest

A life interest or right to accommodation for life IS a granny flat interest if:

- the person ‘pays’ for a life interest or right to accommodation for life, AND

- the life interest or right to accommodation for life is in a private residence that is to be the person’s principal home.

Explanation: In the real estate industry a ‘granny flat’ is the name given to a self-contained flat in someone’s house. A granny flat interest may be in accommodation that is quite different from the real estate definition of a granny flat.

A person who is the owner (or part owner) of property does NOT have a granny flat interest. They have the right to live in the property because of their ownership.

How to value a granny flat interest

There is no market for granny flat interests because they are private family arrangements. The value of a granny flat interest is GENERALLY the same as the amount paid for the interest. This means there is NO deprivation amount.

Example: The value of a granny flat interest is the amount paid (or value of assets transferred) if a person:

- transfers the title of their home

- pays for the construction and fit out of premises, OR

- purchases property in another person’s name in return for a life interest or right to accommodation for life.

In particular cases, where there is a special reason, the SSAct allows a granny flat interest to be valued at a DIFFERENT amount than the amount paid. These particular cases are the EXCEPTION to the rule that the value is the amount paid. The different amount is called the REASONABLENESS TEST.

The REASONABLENESS TEST uses an approximation of actuarial values called the reasonable value conversion factors. SOME examples of cases where the reasonableness test is used are:

- the person transfers title to their home (or purchases property in another person’s name) AND transfers additional assets:

Explanation: Compare the value of the home and the reasonableness test amount. The value of the granny flat interest is the greater of the two amounts.

- the person pays the cost of constructing premises AND transfers additional assets:

Explanation: Compare the cost of constructing the premises and the reasonableness test amount. The value of the granny flat interest is the greater of the two amounts.

- the person is using the granny flat rules to gain a social security advantage:

Explanation: The value of the granny flat interest IS the reasonableness test amount.

The following are some examples of how the granny flat rules apply. These examples are not exhaustive, rather they illustrate how the policy works in some situations.

Example: A person buys property in their son’s name worth $280,000 AND gives the son assets worth $100,000 in return for a life interest in the home (a total of $380,000). The reasonableness test amount is $310,000. The value of the granny flat interest is $310,000 (because this is greater than the $280,000 cost of the new home).

$380,000 − $310,000 = $70,000

$70,000 IS a gift.

Example: A person sells their home and moves into a house already owned and occupied by a family member, paying for a right to accommodation for life. No construction is needed. The value of the granny flat interest is the amount paid UNLESS the amount paid is greater than the reasonableness test amount. Any amount greater than the reasonableness test amount IS a gift.

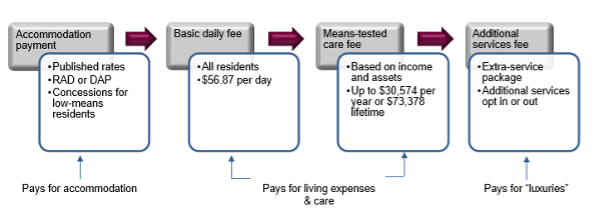

Residential Aged Care

Accommodation payment

You may be asked to pay for your room. The room prices are all published on www.myagedcare.gov.au. You will have the choice to pay a lump sum (refundable accommodation deposit – RAD) or a daily accommodation payment (DAP) or a mixture of both.

Based on your current situation you will be required to pay an estimated RAD of $475,000, which converts to an equivalent DAP of $82.12 per day using the current interest rate of 6.31% per annum.

You will need to check the interest rate applicable at entry. Once determined, it is a fixed rate for the duration of your stay (unless you choose to move to another room).

Payment choices

You can choose to pay your accommodation as a lump sum RAD, or daily DAP or combination of both. You have up to 28 days after signing your Resident Agreement to make this decision.

The service provider may limit how much RAD you can pay within the first 28 days in care by ensuring that you have at least $55,000 in assessable assets after making a payment. If this limit applies, you can pay more towards your RAD once this time-frame has expired.

If you choose to pay the RAD it can be paid from your available income sources or assets or you can ask the provider to deduct the DAP from any lump sum RAD that you have paid. This can help to manage cashflow but will cause your DAP to increase over time in line with the reduction in your RAD balance.

Any RAD paid is fully refundable to you or your estate when you leave. If you have asked the service provider to deduct any fees (including DAP) from the amount held the amount refundable is reduced by the fees deducted. Repayment is guaranteed by the Federal Government provided the service is an approved service provider. DAP payments are not refundable.

The amount paid as a RAD is included when calculating means-tested care fees but is exempt for determining your eligibility for Centrelink benefits.

Basic daily fee

All residents pay the basic daily fee.

It is set at 85% of the single basic age pension (excludes the pension supplement) and is indexed every six months (March and September). The current rate is $56.87 per day.

This fee is a contribution towards your living expenses in care which includes meals, cleaning, laundry, electricity and water services.

Means-tested care fee

If you have assessable income and assets over certain thresholds, you may be asked to contribute more towards the cost of your care through a means-tested care fee (MTF). This reduces how much the government pays on your behalf.

You will need to complete an income and assets assessment to have this fee assessed. If this form is not completed, you may be asked to pay your actual cost of care. In either case, the amount payable is limited to:

- A daily cap of $358.41 per day;

- An annual cap of $30,574 (once reached the MTF reduces to zero for the rest of the year); and

- A lifetime cap of $73,378 (once reached the MTF reduces to zero for the rest of your stay in care).

The means-tested fee is recalculated each quarter and may change in line with changes to rates, thresholds or your financial situation. As you receive a means-tested pension, you will need to notify Centrelink within 14 days of any significant change in your income, assets or personal circumstances. This update includes payments made towards your RAD . This information is used to reassess your fees.

Additional services fees

Your service provider may offer additional services for a fee. This can be on a user-pays basis or a packaged fee. This package may come as part of your room or may be an optional package that you can select.

Examples of additional services could include a choice of meals, daily newspaper, glass of wine or beer with meals, hairdressing, physiotherapy etc.

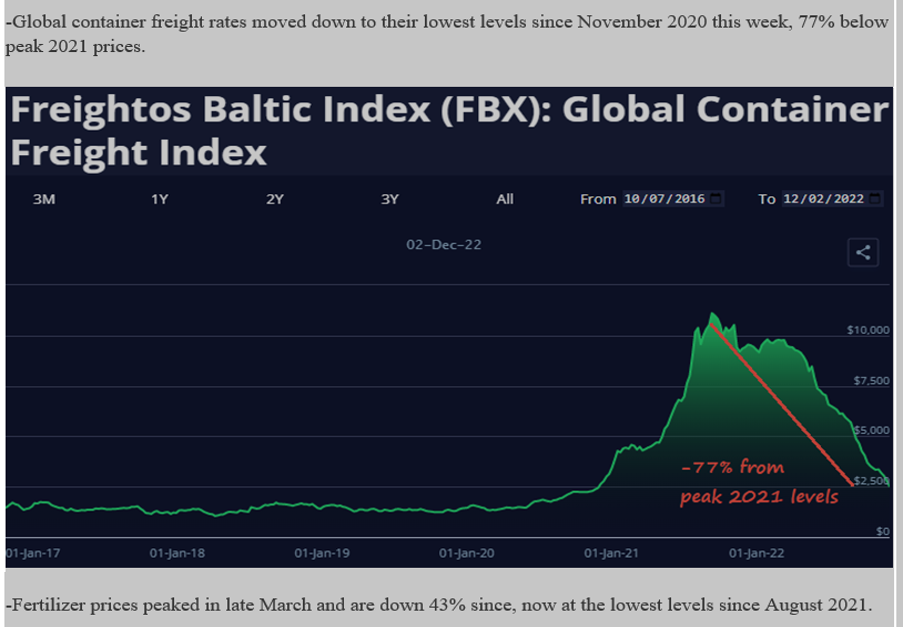

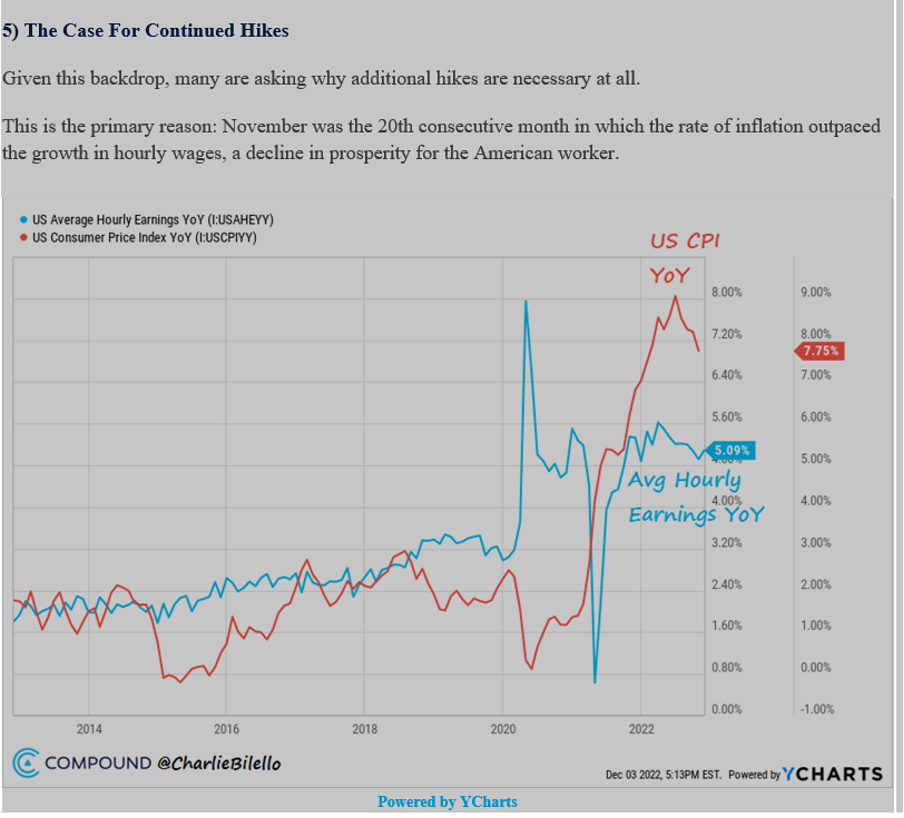

Market Wrap