It could just be me but 2023 was a bit of a blur. I did do a lot of travel, both for work and personally, so that may be part of it, but there did seem to be a lot going on generally.

I probably devour a bit too much sport and this has been a great year to be a couch potato. We had world cups in Netball, Rugby, Cycling, Soccer (Women’s), Aquatic, Basketball and Cricket. When you then mix in the rugby league and AFL with Brisbane teams featuring (unsuccessfully, but let’s not talk about that) in both, that probably added to the channel surfing? Finally, if you like your NBA, sailing and motor racing, those screens at home were working overtime.

Financial markets have also kept us guessing, driven by inflation, and reflected in rapidly increasing cash rates.

- Since May 2022 the Reserve bank has increased the cash rate 13 times, starting from a low of 0.10% and reaching 4.35% on the 7th of November 2023.

- We started 2023 at 3.10% so a rise of 1.25% for the calendar year.

Add to this, the ongoing war in Europe, the terrorist attack by Hamas on Israel and the subsequent response, frictions in the South China Sea with an increasingly belligerent China and a bit of a political shambles for the Albanese government in the second half of the calendar year, and it was very hard to gauge how and when the markets would react.

Suddenly in November, inflation fears in the US and Europe have started to ease and the market has seen that as a very strong ‘buy’ signal.

All markets have not been equal, and the US market has delivered a very different experience to the Australian markets. I will share the Australian investment experience below, which has been less than ideal, as opposed to the strength of the US market, but when history looks back on investments in 2023, it will probably just see a good positive year for a balanced investor, but it didn’t feel like it!

Firstly, The US

The S&P 500 US Index for this calendar year has risen by 20.40% on 8th December andit has been a volatile ride, largely driven by what is now known as the Magnificent 7 (Mag7):

- Alphabet (Google), Amazon, Apple, META (Facebook), Microsoft, Nvidia (Microchips) and Tesla.

In January 2023, the index was at 3824.14 and then climbed to 4588.96 by 31 July (up 20%).

- It then slid, with a few false rallies, until 27 October to 4117.37. A drop of 10.30%.

- Then in November bounced to a new high of 4604.37 (8 December).

The Mag7 accounts for approximately 77% of the index’s rise to 8 December 2023, though they all had significant share price losses in 2022. In short, they were coming off lows, but it was a significant bounce.

- Nvidia for example dropped by 50.3% in 2022. It is up more than 217% for this calendar year.

- Tesla which you may think had a bad year with ‘X’ (previously known as Twitter) dramas and Elon refusing to play nice with advertisers started the year with a share price of $108.10 USD, was at $243.84 USD by 8 December. A rise of 125.6% (back on 5 Nov 2021 it was at $407.36 so still well below previous highs).

Of the Mag 7; Microsoft, Apple, Amazon and Nvidia are above their Nov/Dec 2021 highs and Meta, Alphabet and Tesla are still below, with Tesla being the most significant.

On the upside only 24% of the stocks in the S&P are currently trading within 10% of their all-time highs so there is room for contributions from the rest of the market in 2024.

And Then We Have Australia

In Australia, the All-Ordinaries price index had a very sideways calendar year though it has had its ups and downs. It started the year at 7131.6 and on 8 December was 7405.6. A rise of 3.8%. Unfortunately, it peaked at 7897.70 on the 13th of August, 2021. Still underwater by 6.6%.

Australia generally has not been a great performer:

- Fixed Interest (think government and corporate bonds) only achieved 1.63% for the calendar and actually -1.23% for the rolling twelve months.

- The listed property index was 3.14% for the twelve months to 8 December but is still down over 25% from its high on 31 Dec 2021.

The Exception:

Australian Residential property has been surprisingly solid despite the rate rises.

This is hurting new entrants and rewarding incumbents. Arguably, a big driver for this is foreign buyers as well as net migration of over 510,000 new arrivals in the year to October (Canberra, as a reference, has a population of 472,000 people).

- Median house prices continue to grow with Sydney at $1.125 million. (1 January 2020, pre-covid, it was $973,664). Over the four years that is a 3.9% price growth a year.

- Gold Coast median house prices are now at $901,645.

- Brisbane -South Median price is $1.012m

- Other Queensland property statistics are in this link. https://www.abc.net.au/news/2023-11-09/queensland-property-prices-real-estate-boom/103074314

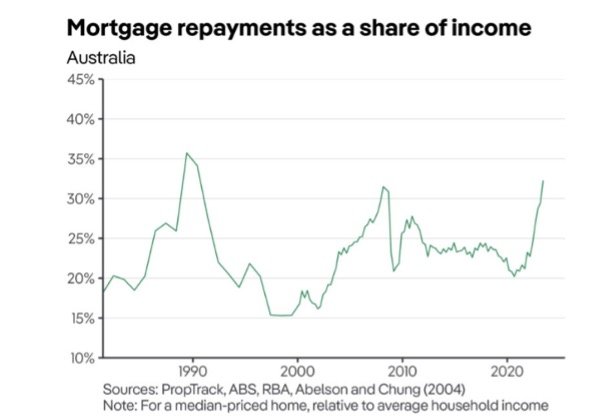

While we are strong advocates for property in a portfolio, we can see headwinds based on current prices. The Government is determined to slow migration which may ease rental pressure later in 2024 and you also need to consider housing affordability and mortgage repayments as a percentage of household income.

Servicing a mortgage is close to as hard as it has ever been in Australia. As per the graph below, 1989 was the previous peak.

Another alarming Australian statistic is based on what percentage of houses sold across the country could have been bought by Australians on median wages. In 2019, 2020 around 40% of households could have been bought by median-income households. In September 2023 this was approximately 13%.

Household earnings of $200,000 a year (which means they are earning more than 80% of Australians) would struggle to buy 50% of the houses sold this year.

Where to from here from Australian Property?

Historically in this sort of market you see prices hold or ease, as Australians are very loathed to sell a property at a loss. Renters stay in rental properties as it is cheaper than buying. Eventually rents catch up and then prices can grow once again.

There are always exceptions, and some forced sellers will take a loss to sell and renters may increase their incomes allowing them to buy, but generally, properties can stagnate when prices are stretched and this is not unusual late in the property investment cycle.

THE PROPERTY INVESTMENT CYCLE

So, what can we look forward to in 2024?

For those still in fixed interest rate loans, you may have seen the worst of the rises and you may have some relief before you negotiate that variable rate. We have the advantage of watching inflationary pressures ease in the US to give us an indication of what will happen here.

- Supply chain issues are reducing and this rain should be helping our farmers. Building costs and household groceries could benefit from those reduced costs.

- The currency has strengthened recently, which should reduce the cost of imported manufactured goods.

- Oil prices have reduced steadily since 6 June 2022, when it peaked at $118.50 USD per barrel. The current price (on 11 December 2023) is $71.23 USD per barrel. That is down by almost 40%. There was a brief bounce back to $93.68 in late September but since then it has softened. We should see this impact at the bowser but it also reduces costs on anything that needs to be transported.

- Our currency back in May 2021 was 78 cents to the US dollar and has been as low as 63 cents in late October but is now back at 66 cents. If US interest rates reduce we could see the currency strengthen as the differential between our cash rates (4.35%) and the US cash rates of 5.5% has been a big reason for the US dollars strength.

- Australia continues to run $7 billion plus monthly trade surpluses (though down from the $14.6 billion surplus back in March 2023) so those surpluses should finally be reflected in the currency.

The cost-of-living pressures will then be largely tied to government fiscal policies and the government will need to find ways to rein in spending and the growth in the public service.

If we do see a migration reduction, housing stresses may ease so prices can normalise and building could return to the numbers we saw in FY2019. That year over 197,000 new homes were built. Currently for the 24_25 Financial Year (FY) the forecast is only 178,000.

- To increase that number we would need banks to be motivated to lend to developers and possibly ease some of their more onerous lending policies. Additionally, developers would need local governments and councils to provide access to new sites and reduce red, green and indigenous tape.

- Net migration is now ‘meant’ to be coming down to 375,000 in 2023_24 and then 250,000 in 2024_25.

- New property stock would be hard pressed to meet the 23_24 migration numbers but by 24_25 it may provide relief.

The Australian share market has a large exposure to financial and resource stocks and that may shackle performance a little in 2024 but many of the top 200 shares in the All Ords look quite healthy. The recent downturn has shed highly leveraged companies which were already at risk, leaving the balance well placed to participate in any improvement in consumer sentiment.

We can start 2024 cautiously optimistic, which wasn’t where we were in January 2023. Back then we were just ‘cautious’.

- There will be a US election and the Middle East and Ukraine are a long way from any settlement but they are known unknowns.

Our job is not necessarily to predict the future, but to plan for it.

A few things that you will know on January 1, 2024:

- Australia is one of the least polluted countries in the world sitting at number 8. All the other countries in the top 10 have populations of less than a million people.

- Australians are among the richest people in the world with the median net worth of an Australian adult more than US$273,000 when we include property and shares.

- Australia has the highest solar power installation per capita in the world and creates more energy from solar per capita than anywhere in the world. Even on a cumulative basis against much larger countries, Australia ranks number six in total energy produced by solar (30 Gigawatts).

- Australia’s CO2 emissions peaked in 2010 at 415.3 million metric tonnes. In 2022 this was 393.16 million metric tonnes, down by 5.2% despite increasing the population by 20% through the same period.

- In its 36 years of recorded history, the Great Barrier Reef now has its highest-ever hard coral coverage so get your snorkel and flippers out and go and enjoy it.

We won the DNA lottery by being born Australian and we should never take that for granted.

To you and yours, we wish you a very Merry Christmas and a happy and prosperous new year and as always, if you have any concerns, please do not hesitate to contact us.

Merry Xmas

Paul Forbes, RFS Advice CEO